The self-storage sector is entering 2025 with mounting evidence of a cyclical upswing. After a period of pandemic-driven highs followed by a modest correction, key indicators now signal that a rebound is underway. For both high-net-worth accredited investors and newcomers exploring their first real estate syndication, self-storage presents a confident, data-supported case for renewed growth. This article from Signal Ventures breaks down why smart capital is moving into self-storage now – before the broader market catches on – and why early positioning could be strategic.

From Boom to Slowdown: A Resilient Sector Finds Its Floor

Self-storage enjoyed unprecedented demand during the 2020–2021 period, but by 2023 the market faced headwinds. Elevated supply growth and a cooldown in moving activity (a primary demand driver) led to softer fundamentals. Property values pulled back roughly 20% from their 2021 peak, according to Green Street data. Occupancies, which had been in the mid-90% range at the pandemic peak, dipped back toward historical norms around the low 90s. National average occupancy in 2023 was about 91–92%, down a couple of percentage points from the prior year. Rental rates also retreated: industry-wide, street rents fell approximately 10% in 2023 after the COVID surge. Heavily supplied Sunbelt markets saw sharper rent declines (often in the 10–15% range), while dense coastal cities held steadier. In short, by late 2024 the sector had undergone a healthy correction, digesting new supply and reverting from unsustainably high COVID-era demand.

Crucially, even during this slowdown, self-storage proved its resilience relative to other property types. Investors continued to view storage as a “safe haven” in a volatile CRE environment, transacting $3 billion in U.S. self-storage property sales during 2024 (over 800 facilities traded). The asset class maintained consistent cash flows despite rising interest rates and inflation. Cap rates (initial yields) stayed roughly flat through 2024 even as values dipped, reflecting investor belief in the sector’s long-term stability. In other words, the foundation held firm: occupancy levels, though off their highs, remained healthy, and savvy investors quietly started to accumulate assets at discounted prices.

Early Signs of Stabilization in 2024

By late 2024 and early 2025, data began to show that the self-storage market had found its footing. The downward trend in rents is losing steam and even starting to reverse. In January 2025, the national average self-storage rent was only 0.7% lower than a year prior, a far smaller year-over-year drop than earlier in 2024 7 . More significantly, rents rose about 0.8% month-over-month in January – an unusual feat in what is typically the slow season. Likewise, April 2025 figures show national self-storage rents down a mere 0.4% year-over-year, essentially flat, with a return to sequential monthly growth heading into spring. In fact, 27 of the top 30 metro markets saw rents increase between March and April 2025. Markets like Chicago, Tampa, and Washington D.C. are now posting annual rent gains of 2–3%, reflecting constrained supply and sustained demand in those areas . The worst-performing cities (e.g. Austin, San Diego) are still seeing declines, but even those are moderating to single-digit percentages. This broad-based stabilization suggests the sector is at an inflection point.

Occupancy rates tell a similar story. After ticking down from record highs, occupancies have largely plateaued at healthy levels, rather than spiraling further down. By Q4 2024, average occupancy at major self-storage REITs hovered around 91%, only slightly below the prior year. Essentially, facilities on the whole stopped losing tenants – a clear sign that demand has caught up to the new supply delivered in recent years. Industry observers note that “flat occupancy trends suggest the worst may be over”. Many operators used aggressive promotions in 2023–24 to keep occupancy up, accepting a temporary dip in revenue growth to retain customers. That strategy appears to have paid off: the customer base has largely stabilized, and now rental rates can be inched back up. Net operating income (NOI) trends, which were slightly negative in 2024, are expected to turn positive again in 2025 as the combination of steady occupancy and improving rents kicks in.

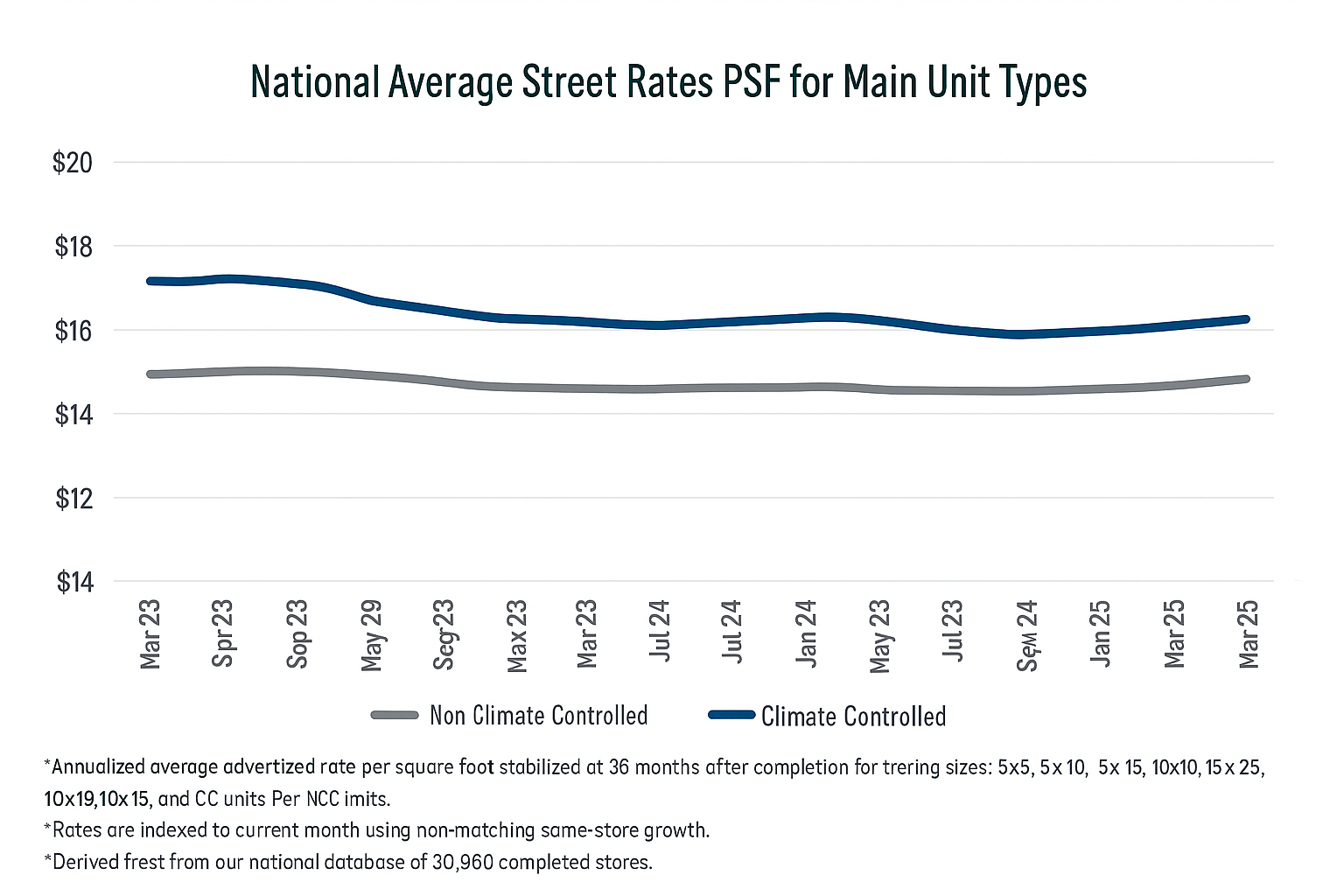

National average street rates (per square foot) for self-storage units trended downward through 2023 but began rebounding modestly in 2024–2025, as shown above. Both climate-controlled (blue) and non-climate (gray) unit rates have firmed up after a period of decline (data through May 2025). The inflection in this rent curve is a key marker of the sector’s stabilization.

The macroeconomic backdrop is also becoming more favorable. The Federal Reserve’s aggressive rate hikes in 2022–2023 – which had cooled the housing market and self-storage demand – have given way to a more stable outlook. By early 2025, interest rates have plateaued, with the Fed even signaling potential rate cuts on the horizon 15 . While high borrowing costs in 2024 put a damper on self-storage development and transactions, the mere expectation of easing rates has improved investor sentiment. Consumer price inflation, which was running hot in 2022, has moderated in 2024, restoring some consumer confidence. Self-storage operators report improved leasing velocity as renters adjust to the new normal and feel more secure in their finances 15 . In short, the clouds are parting: with the economy on a stable footing (no recession materialized in 2024) and interest rate pressure likely past its peak, the stage is set for self- storage fundamentals to strengthen.

Demand Drivers: Mobility, Housing, and Lifestyle Shifts

One of the strongest indicators for self-storage demand is housing mobility – people moving households. Over the past two years, the U.S. saw an unusually low level of moving activity, which directly dampened storage usage. Why the slowdown? One factor is the housing market lockdown effect: roughly 56% of U.S. mortgage holders have interest rates below 4%, a byproduct of the ultra-low rates in 2020–21. With market mortgage rates now around 6–7%, homeowners have been reluctant to sell and lose their cheap loans. Fewer home sales means fewer moves, which in turn meant less demand for storage units (moves typically account for about 50% of self-storage usage). This dynamic, combined with high home prices keeping many first-time buyers sidelined, led to 2024 home sales hitting their lowest level in nearly 30 years. Industry analysts estimate that the drop in moving activity contributed to roughly a 10% decline in storage demand in the recent down cycle.

The good news: this trend appears to be reversing. By late 2024, the decline in home sales had stabilized and even showed a slight uptick. Historical patterns (and common sense) suggest that people can only postpone life changes for so long – pent-up demand for housing and relocation is building. As mortgage rates eventually ease, even marginally, more homeowners will be willing to move, and more buyers will re-enter the market. Home buying is expected to increase in 2025, and with it, storage rentals to facilitate those moves. In fact, Argus Self Storage Advisors projects that an uptick in home sales, along with improving consumer sentiment, will help industry occupancy bounce back by 200–400 basis points (2–4%) by the end of 2025. Simply put, more people moving equals more demand for that convenient 10×10 storage unit during life’s transitions.

Demographic and lifestyle shifts further bolster the long-term demand story. Americans are, on average, living in smaller spaces and renting homes more than ever – both positive indicators for self-storage usage. The average size of new U.S. homes has shrunk about 12% since 2016, reflecting trends toward urban living and affordability constraints. At the same time, a record 36% of Americans are renters rather than homeowners. This matters because renters are 2–3 times more likely to use self-storage than homeowners, often due to having less space or needing to move more frequently. The convergence of smaller living spaces and a growing renter population points to a sustained baseline demand for storage that is structurally higher. Even independent of big life events, many people simply need a “third closet” or a flexible space for belongings that don’t fit at home.

Commercial demand drivers add another layer. Small businesses and entrepreneurs increasingly utilize self- storage units as cost-effective micro-warehouses, inventory storage, or operations hubs. During economic transitions (like an inflationary period or post-COVID adjustments), businesses might downsize offices or seek cheaper storage for files, equipment, or excess stock. Self-storage fulfills this need on flexible terms. Inflation can actually spur storage demand in this segment: as retail or industrial rents rise, companies look for more affordable overflow space – and climate-controlled storage units can fit the bill. On the residential side, during times of economic uncertainty, people often declutter or downsize to save money, which boosts demand for storage units to hold overflow possessions. These behavioral trends mean that storage demand isn’t solely tied to boom times; it has counter-cyclical aspects as well.

Supply Side: Development Pipeline Hits the Brakes

While demand is rebounding, new supply is finally tapping the brakes – a crucial ingredient for a market upswing. One reason self-storage experienced a lull was a wave of new construction that hit in 2018–2022. Developers, attracted by the sector’s strong performance and relatively low entry costs, built aggressively, especially in high-growth metros. By some estimates, total U.S. storage inventory grew by ~8–9% over just the past three years. This building boom overshot demand in certain cities, leading to localized oversupply and price competition. However, starting in 2022, multiple forces slammed the brakes on new projects. Rising interest rates and higher construction costs made it far more expensive to develop facilities. At the same time, softening rental rates and occupancy meant new projects penciled out less favorably. According to industry analyst Cory Sylvester, the number of new self-storage openings in 2023 fell to less than half the average of the previous five years. Many developers literally shelved projects or sold off entitled land rather than breaking ground, preferring to wait for a better climate.

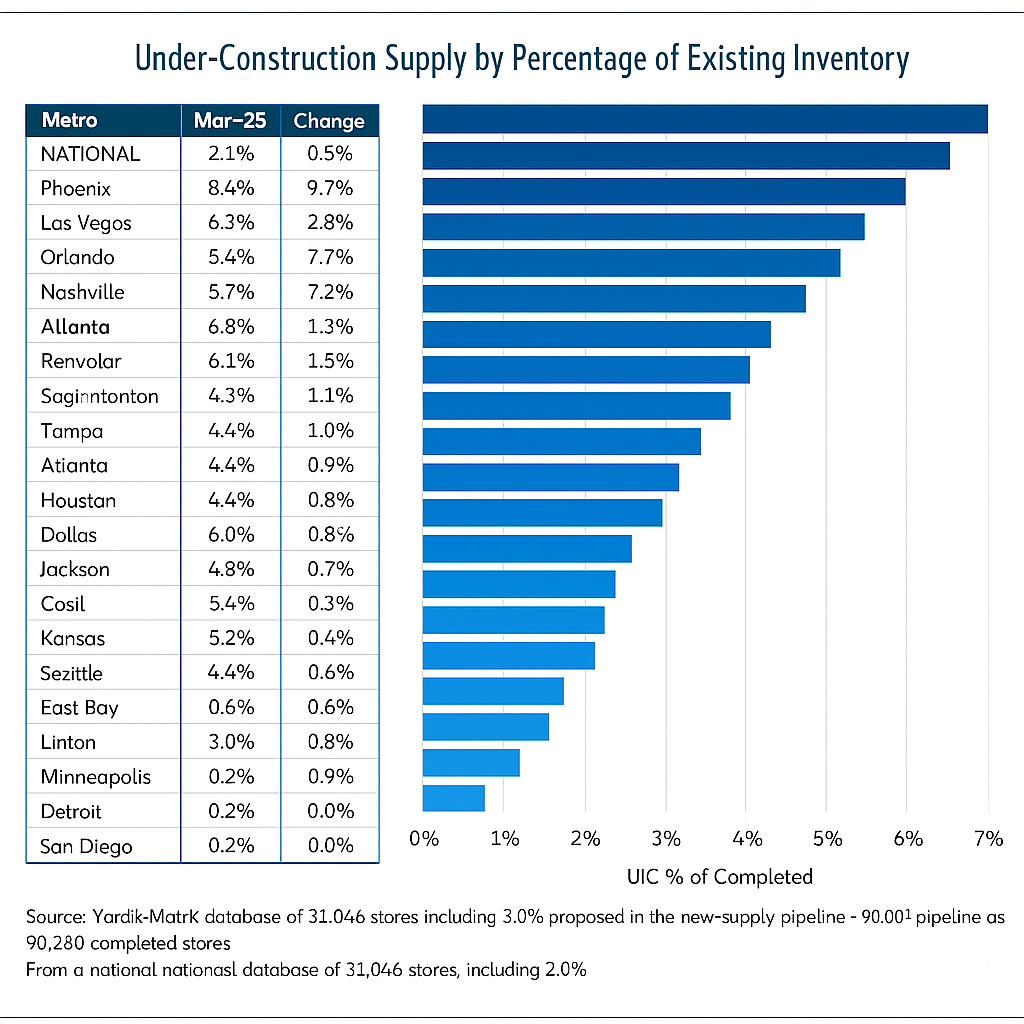

Now, in 2025, the development pipeline has materially thinned. At a national level, only about 2.8% of existing self-storage inventory is under construction (as of April 2025), down from over 4% at the peak of the building wave. Research from Yardi Matrix and others shows the pipeline dropping each month – a trend projected to continue into 2026. In fact, forecasts suggest that new supply additions will decline ~15% in 2025, and another 18% in 2026. Developers are cautious, lenders are tighter with financing, and the projects that do proceed are often smaller or in underserved markets. This pullback in construction is a classic cyclical response and a healthy one: it allows existing facilities to absorb demand and push rents without fear of a new competitor opening down the street. Markets that were hit hardest by oversupply (for example, Phoenix, Dallas, parts of the Southeast) are finally seeing relief, as very few new facilities are slated in the next year or two relative to those markets’ size.

New facility construction is slowing across the country. The chart above shows the under-construction supply as a percentage of existing inventory in major metros (April 2025 vs. March 2025). Nationally, the pipeline is down to about 2.8% of stock. Oversaturated markets like Phoenix and Las Vegas still have relatively high construction levels (5–6% of inventory under construction), but many markets are well below 3%. Fewer new deliveries in 2025–2026 will help rents recover, especially in cities where development had been rampant.

Notably, even the projects counted as “under construction” in 2025 may not all reach completion on schedule – some could be delayed or canceled if economic conditions shift. The cost of capital remains high, and construction material costs, while off their peak, are still elevated compared to pre-pandemic. This means only the most compelling projects (in high-barrier locations or with exceptional demand cases) are moving forward. The practical impact for investors is a window of reduced competition: for the next couple of years, most markets will get a breather from new supply. In the long run, supply will respond to improvements – the development pipeline can reload quickly once rents and occupancies rise enough. But that response typically lags 18–24 months. Today’s investors have a strategic opportunity to acquire or develop facilities now, ride the demand recovery, and enjoy improving cash flows before the next wave of supply eventually comes. By the time developers ramp up again, early investors could be locked into favorable bases and potentially even capture upside from cap rate compression as market optimism returns.

Institutional Capital is Betting on a Rebound

Perhaps the strongest vote of confidence in self-storage’s next cycle is the behavior of institutional investors and industry leaders. While some observers were focused on the short-term dip, seasoned players have been quietly doubling down on the sector. In 2024, even as operating metrics cooled, major acquisitions and partnerships accelerated – a telltale sign that “smart money” sees value. Public Storage (the largest storage REIT) made headlines with a $2.2 billion acquisition of Simply Self Storage from Blackstone in mid-2023. Around the same time, Extra Space Storage (another REIT) completed a $12.7 billion merger with Life Storage, consolidating two of the industry’s biggest operators. These blockbuster deals underscore how the top players were positioning for long-term growth, essentially using the period of softer performance to expand their portfolios at scale. As one industry CEO noted, some pandemic-era demand may have waned, but that only opened the door for more consolidation in a fragmented sector.

The trend continued through late 2024. Private equity and well-capitalized investors have remained highly active, particularly in secondary markets where pricing became attractive. By year-end 2024, transaction volume was clearly on the upswing – sales in the second half of 2024 were estimated to be up 50% compared to the first half. All told, investors poured over $3B into self-storage acquisitions in 2024, purchasing more than 51 million square feet of storage across 822 facilities. The roster of buyers includes some of the savviest names in real estate. For example, Prime Group Holdings (a major private storage operator) acquired over $260M in assets in 2024, and Carlyle Group (a global private equity firm) put about $178M into self-storage deals. Even institutional capital known for its discipline is getting involved: CubeSmart, a publicly traded REIT, formed a joint venture with Hines (a global real estate firm) in early 2025 to recapitalize a 14-property portfolio in Dallas-Fort Worth 14 . In that deal, CubeSmart invested roughly $160 million for an 85% stake, signaling confidence in key growth markets and high-quality assets. Moves like these highlight that big players are not waiting on the sidelines – they’re actively buying in before the wider market perceives the recovery.

Why the rush? One reason is valuation and timing. As noted, storage asset values corrected downward in 2023–24, creating a more attractive entry point. For investors with dry powder, this is an ideal moment to acquire assets at a relative discount – effectively “buying low” in anticipation of the next “high.” Signal Ventures and other forward-looking firms recognize that once rent growth and occupancy gains show up consistently in quarterly earnings, everyone will want in, likely driving prices up. By moving early, an investor can capture the upside as net operating incomes improve, and potentially benefit from cap rate compression (i.e. rising asset values) as the sector swings back into favor. As one Colliers report put it, institutional demand for self-storage remains strong even in the interim, because the fundamentals are expected to turn positive and justify those investments. Storage has a track record of quick performance recovery after soft patches, which gives confidence to those with a longer-term horizon.

Another factor is that storage has proven itself through the cycle, strengthening its reputation. During the pandemic and subsequent inflationary period, self-storage was one of the best-performing real estate asset classes. It had very low loan default rates and maintained high occupancy, whereas sectors like office and retail suffered severe distress. This resilience is not lost on large investors. Many institutions that historically focused on apartments, office, or industrial properties are now increasing their allocations to “alternative” sectors like self-storage, seeking diversification and stable yields. As of 2024, the four largest self-storage REITs owned only about 30% of the U.S. storage inventory (up from 17% in 2000) 37 – indicating plenty of room for further consolidation and institutional ownership growth. Large capital inflows, such as new funds targeting storage or REITs raising investment capital, often presage a sector upswing. Indeed, market experts forecast robust acquisition activity in the latter half of 2025, with both private investors and REITs looking to capitalize on improved conditions.

For individual investors or smaller syndicates, the key takeaway is that “smart money” is already positioning itself. When you see seasoned industry players expanding holdings and heavyweight financiers entering joint ventures, it’s a strong vote of confidence in the sector’s next chapter. These investors are not speculating on hype; they’re reacting to concrete metrics – stabilizing rents, easing supply pressure, and historically proven demand drivers – all of which indicate a coming upswing. Following their lead (with proper due diligence) can potentially allow smaller investors to ride on the coattails of institutional strategy, benefitting from the groundwork they’ve laid and the market momentum they anticipate.

Inflation Resilience and Cash-Flow Appeal

Inflation and rising costs have been top-of-mind for many investors recently. Here again, self-storage shines in ways that support its 2025 comeback narrative. Self-storage is often viewed as an inflation-resilient asset class. Why? Unlike property types with multi-year leases (think office towers or shopping centers), self-storage rentals are typically month-to-month agreements . Owners can adjust rental rates quickly– even several times per year – in response to market conditions. During an inflationary period, this flexibility means storage operators can raise rents in real-time to keep pace with rising prices, helping protect or even boost their revenue in nominal terms. We saw this in practice in 2021–2022 when many storage REITs implemented multiple rate increases as consumer prices climbed, effectively passing inflation through to customers. Even now in 2025, with inflation moderating, the ability to nudge rates upward contributes to the recent rent recovery. The short lease structure is a built-in hedge: storage landlords are never stuck with below-market rents for long.

Moreover, the cost side of the equation in self-storage is relatively favorable. Self-storage facilities are simple to operate – no lavish lobbies, minimal maintenance compared to apartments, and often only 1–2 staff members per property. As a result, the operating expense ratio for storage typically ranges only 25%–40% of revenue, far lower than most other real estate sectors. This lean cost structure means that even if some expenses (utilities, insurance, property taxes) rise with inflation, the impact on the bottom line is limited. A small increase in revenue can offset a large percentage jump in expenses. In fact, many operators are mitigating cost pressures by embracing tech and automation (e.g. remote leasing, kiosks) to keep payroll and office hours lean . High inflation also tends to increase replacement costs(construction prices), which can raise the barrier for new competition – a silver lining for owners of existing facilities.

On the demand side, as mentioned, inflationary times can trigger behaviors that inadvertently favor self- storage. When prices for housing, goods, and services rise, consumers often re-evaluate their space needs and consumption. Some will downsize to smaller dwellings to save on rent or mortgage, using self- storage as a relief valve for the stuff that no longer fits. Others might delay buying a larger home (sticking it out in a starter home or apartment), again creating overflow storage demand. Small businesses facing higher rents might give up storefronts or warehouses and shift operations partly into storage units (a trend seen with online entrepreneurs and contractors). In these ways, storage demand has shown an ability to hold up or even get a bump when economic conditions are in flux. This was evident during the COVID-19 shock and the inflation surge that followed – storage occupancy remained solid while usage patterns shifted (people storing office equipment during work-from-home, etc.).

Overall, the inflation resilience of self-storage adds to its appeal for investors seeking stable cash flow. Even if inflation remains somewhat elevated into 2025, storage investments are positioned to weather it. Rental income can be frequently adjusted upward, and the intrinsic value of hard assets like storage facilities tends to rise in inflationary periods (land and building costs go up, which usually supports property values). In real terms, this helps preserve the investor’s purchasing power. For a portfolio looking to hedge against inflation while also generating income, self-storage hits a sweet spot – a fact not lost on the institutional players driving capital into the sector.

Early Positioning for Upside

All the pieces are in place for a strategic comeback in self-storage. The sector has navigated its downturn and is showing concrete signs of a rebound: occupancies have stabilized, rents are recovering, new supply is constrained, and demand catalysts are strengthening. Equally important, the investor community – from REITs to private equity to family offices – is voting with its dollars in favor of this asset class. But the window of opportunity won’t stay propped open forever. Early 2025 represents a unique timing sweet spot where the data is pointing upward yet broad market sentiment hasn’t fully caught up. For investors, this is often the moment to strike – before cap rates compress and competition intensifies.

Consider the likely scenario over the next 12–24 months: As 2025 progresses, we expect to see modest same-store revenue growth returning for the major self-storage operators. Quarterly earnings releases from the REITs will start to show positive rent growth again, and occupancy may even tick up a bit. By late 2025, if forecasts hold, rental rates in many markets could be growing in the low-to-mid single digits annually. Once the broader market observes a couple of quarters of improved metrics, sentiment will shift from “cautious optimism” to “bullish.” At that point, asset pricing is likely to move – sellers will feel more confident in raising asking prices, and buyers, flush with improving debt terms (should interest rates fall), will be willing to pay more. The generous buyer’s market of 2023–24 for self-storage could transition to a seller’s market by 2026 if fundamentals accelerate. Early investors stand to capture value uplift during this swing. Those who waited on the sidelines risk finding that the “easy gains” (from buying at distress or trough pricing) have already been taken.

Early positioning also allows investors to be choosier and more strategic. Right now, there are still pockets where one can acquire high-quality storage properties at reasonable yields, especially in secondary markets or as part of off-market deals. As the cycle heats up, the best opportunities tend to get picked over quickly. By moving in 2025, an investor can lock in assets with the knowledge that the wind is at their back, then potentially refinance or exit in a stronger market a few years down the line. It’s a classic case of skating to where the puck is going, not where it currently is. The fact that development is limited in the near term means any investments made now have a clearer runway to perform without immediate new competition. Furthermore, any incremental improvements (e.g. raising below-market rents, adding tenant insurance sales, etc.) will coincide with a rising market tide, amplifying returns.

At Signal Ventures, we interpret these converging trends – stabilized fundamentals, favorable supply/ demand dynamics, and increased institutional bullishness – as a signal (no pun intended) that now is the time to lean into self-storage opportunities. Our perspective is strictly data-driven and educational: whether you’re a seasoned accredited investor or exploring your first private real estate deal, the numbers tell a compelling story. Self-storage in 2025 is not about speculative growth; it’s about a proven sector coming off a controlled reset and entering its next expansion phase. As always, thorough due diligence and market selection are key (not every facility or location will outperform, and local conditions vary). But the national outlook is one of cautious confidence turning into optimistic momentum.

Conclusion: Positioning for the Self-Storage Upswing

Few real estate sectors offer the combination of recession-tested resilience and renewed growth potential that self-storage does as we head into 2025. The industry’s short-term challenges – from a temporary demand dip to an oversupply hangover – are giving way to improving metrics across the board. Occupancies are firm, rents are inching up, and new development is in check. Macroeconomic winds are becoming more favorable, with housing mobility set to improve and inflationary pressures that self-storage can adeptly handle. Perhaps most telling, the sophisticated capital is already on the move: major investors are increasing allocations to storage, betting on a rebound before the crowd fully arrives.

For investors evaluating their next move, the self-storage sector deserves a close look. The case for a strategic comeback is supported by hard data and current trends, not hype. Early movers who act on these insights stand to benefit from buying into a recovering market with significant tailwinds. Whether you’re aiming to diversify your real estate portfolio or seeking a first foray into private syndications, self- storage offers an accessible, well-understood business model with upside on the horizon.

At Signal Ventures, we’re excited about what 2025 holds for self-storage and are committed to sharing knowledge on this sector’s dynamics. We invite anyone interested in learning more – be it understanding the latest market reports, exploring partnership opportunities, or simply getting expert perspectives – to connect with us or follow up for additional insights. The rebound in self-storage appears to be underway, and being educated and engaged now is the key to staying ahead of the broader market. In the world of smart real estate investing, recognizing the cycle’s turn and positioning early can make all the difference. Here’s to informed decisions and capitalizing on the strategic comeback of self-storage in 2025.

References:

Storage Market Set to Recover in 2025 – Knowledge Leader – Commercial Real Estate Content Hub

https://knowledge-leader.colliers.com/aaron-jodka/storage-market-set-to-recover-in-2025/

Self Storage Industry Statistics (2024) – Neighbor Blog https://www.neighbor.com/storage-blog/self-storage-industry-statistics/

Investors Poured $3B Into Self-Storage in 2024 – CRE Daily https://www.credaily.com/briefs/investors-poured-3b-into-self-storage-in-2024/

2025 Kicks Off With Cautious Optimism In The Self Storage Sector https://www.rentcafe.com/blog/self-storage/self-storage-report-february-2025/

Self Storage Market Trends Show Stabilization In 2025 – CRE Daily https://www.credaily.com/briefs/self-storage-market-trends-show-stabilization-in-2025/

Self Storage National Report – November 2024 – Multi-Housing News https://www.multihousingnews.com/self-storage-national-report-november-2024/

SmartStop Self Storage REIT, Inc. Reports Fourth Quarter 2024 … https://investors.smartstopselfstorage.com/news-and-events/press-releases/press-releases-details/2025/SmartStop-Self-Storage- REIT-Inc.-Reports-Fourth-Quarter-2024-Results/default.aspx

Self-Storage Faces Challenges But Shows Signs of Stabilization – CRE Daily https://www.credaily.com/briefs/self-storage-faces-challenges-but-shows-signs-of-stabilization/

Outlook – by, Ben Vestal of Argus Self Storage Advisors – List Self Storage https://listselfstorage.com/industry-insights/2025-outlook-by-ben-vestal-of-argus-self-storage-advisors/

The State of the Self-Storage Market in 2025 and Why I’m Optimistic About Its Future https://www.insideselfstorage.com/market-conditions/iss-blog-the-state-of-the-self-storage-market-in-2025-and-why-i-m- optimistic-about-its-future

How Does Inflation Affect Storage Investments? – Toy Storage Nation https://toystoragenation.com/2024/01/26/how-does-inflation-affect-storage-investments/

Self Storage Market Outlook – October 2024 | Yardi Matrix Blog https://www.yardimatrix.com/blog/self-storage-market-outlook-october-2024/

Public Storage to acquire Simply Self Storage for $2.2 billion | Reuters https://www.reuters.com/markets/deals/public-storage-acquire-simply-self-storage-22-bln-2023-07-24/

Unpacking self storage: A sector on the move https://www.cbreim.com/insights/articles/unpacking-self-storage-a-sector-on-the-move